Executive Summary

Federal marijuana rescheduling changed in April 2026, but the change is limited and narrower than many cannabis businesses may assume.The verified federal action placed FDA-approved marijuana products and marijuana subject to qualifying state-issued medical marijuana licenses into Schedule III. It did not legalize marijuana nationwide, did not automatically include adult-use cannabis businesses, and did not settle every tax or compliance question for operators.

For qualifying state-licensed medical marijuana operators, the action may create important federal tax and compliance implications, especially around DEA registration and Section 280E. But Treasury and IRS have indicated that additional tax guidance is expected, which means operator-specific tax treatment remains partly unresolved.

The safest reading is narrow: this is a limited medical-category federal scheduling action, not full marijuana legalization and not blanket relief for every cannabis business.

Verified Legal / Regulatory Foundation

The April 2026 action sits inside the federal Controlled Substances Act scheduling framework. The Ground Zero packet identifies the Controlled Substances Act, 21 U.S.C. §811, 21 U.S.C. §812, the April 28, 2026 Federal Register final rule, the DOJ April 2026 announcement, 21 CFR Part 1301, IRC §280E, Treasury / IRS tax guidance, and the April 28, 2026 Federal Register hearing notice as the legal and regulatory anchors for this article.

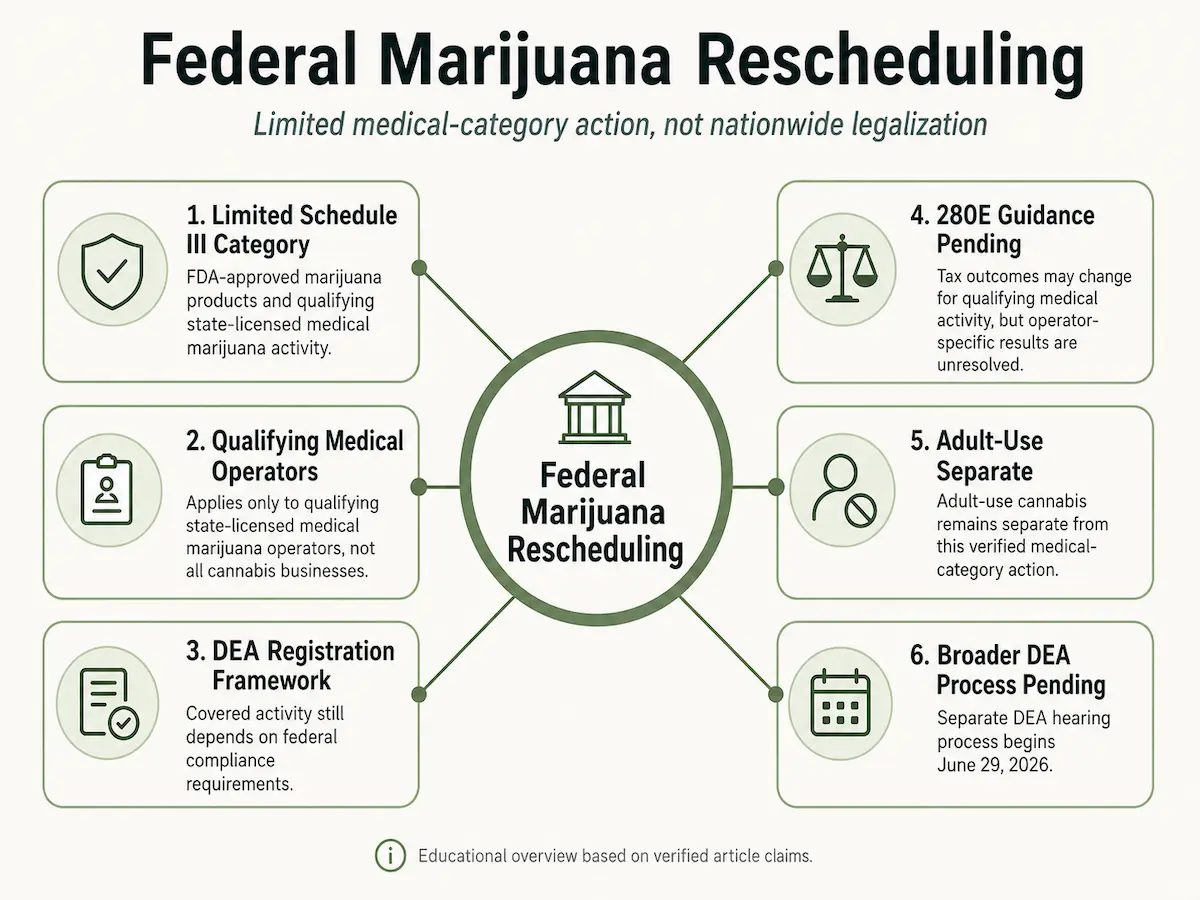

The Federal Register April 28, 2026 final rule created a limited Schedule III category for FDA-approved marijuana products and marijuana tied to qualifying state medical marijuana licensing.

That does not mean all marijuana is now Schedule III. The verified rule applies only to covered medical categories.

The DOJ April 2026 announcement treated the limited medical-category action and broader marijuana rescheduling as separate processes. The broader rescheduling process remains pending through a separate DEA hearing track scheduled to begin June 29, 2026.

The Treasury / IRS April 23, 2026 announcement also matters because Treasury and IRS stated that additional tax guidance is planned after DOJ’s final order on medical marijuana rescheduling. That means the rule may affect Section 280E treatment for qualifying medical marijuana activity, but the rule alone should not be treated as settling every operator-specific tax question.

Confirmed Facts

DOJ and DEA issued an April 2026 action affecting specific medical marijuana categories. The action applies to FDA-approved marijuana products and marijuana subject to qualifying state-issued medical marijuana licenses.

The Federal Register final rule was published April 28, 2026.

The action does not legalize marijuana nationwide.

Adult-use cannabis remains separate from the verified medical-category action. Adult-use-only cannabis businesses are not verified as covered. Recreational marijuana sales are not verified as covered. Dual medical/adult-use operators remain a mixed and unresolved category.

DEA registration is part of the compliance framework for covered activity. However, DEA registration should be treated as a compliance framework issue, not as a guarantee, shield, or legal advice.

Section 280E tax consequences are a major operator issue. Section 280E applies to Schedule I and Schedule II trafficking, so Schedule III treatment may affect qualifying medical marijuana activity. However, Treasury and IRS have indicated that additional guidance is expected.

Retroactive 280E relief is not confirmed.

Banking or FinCEN consequences are not verified as changed.

Hemp is not affected by this marijuana rescheduling action. This action concerns marijuana categories under federal scheduling. It does not reschedule hemp.

Synthetic THC is not covered by this specific rule.

Broader marijuana rescheduling remains separate and pending. The DEA hearing on broader rescheduling is scheduled to begin June 29, 2026.

Clarifications / Misinterpretations

The most important clarification is that federal marijuana rescheduling did not make marijuana federally legal nationwide. The verified material supports only limited Schedule III treatment for covered medical categories.

It is also not accurate to say that all cannabis businesses benefit from the April 2026 action. The action applies to FDA-approved marijuana products and marijuana subject to qualifying state-issued medical marijuana licenses. Adult-use businesses are not verified as covered.

It is not accurate to say that all medical marijuana operators automatically qualify. The correct wording is qualifying state-licensed medical marijuana operators.

It is not accurate to say that Section 280E is gone for all cannabis businesses. The Schedule III action may change Section 280E treatment for qualifying medical marijuana activity, but Treasury and IRS have indicated that additional guidance is expected, especially for businesses with mixed activities.

It is not verified that retroactive 280E relief has been granted.

It is not verified that banking or FinCEN rules have changed because of this action.

DEA portal details should also be handled carefully. DEA registration is part of the framework, but exact portal fees, deadlines, and instructions were not fully confirmed from DEA materials in the Ground Zero packet. Operators should check official DEA materials before relying on practical registration details.

Structural Implications

For qualifying state-licensed medical marijuana operators, the April 2026 federal marijuana rescheduling action creates a new federal compliance and tax environment, but not a complete federal legalization framework.

The first structural implication is category separation. The rule distinguishes FDA-approved marijuana products and qualifying state medical marijuana activity from marijuana activity outside those categories. Operators should not assume that a state cannabis license, by itself, places all business activity inside the verified Schedule III category.

The second structural implication is medical versus adult-use separation. The verified action separates qualifying medical marijuana activity from adult-use cannabis. Benefit claims tied to Schedule III treatment should not be extended to adult-use-only cannabis businesses.

The third structural implication is tax uncertainty. Section 280E is central because it applies to Schedule I and Schedule II trafficking. A Schedule III placement may affect qualifying medical marijuana activity, but Treasury and IRS plan additional guidance. Broad tax conclusions remain unsafe, especially for mixed medical/adult-use operators.

The fourth structural implication is federal registration. DEA registration is part of the compliance framework for covered activity. But DEA registration should not be framed as a guarantee of protection, legal immunity, or a complete compliance answer.

The fifth structural implication is timeline separation. The April 2026 medical-category action is separate from broader marijuana rescheduling. The broader process remains pending, with a DEA hearing scheduled to begin June 29, 2026.

Conclusion

Federal marijuana rescheduling in April 2026 is significant, but limited. The verified action placed FDA-approved marijuana products and marijuana subject to qualifying state-issued medical marijuana licenses into Schedule III.

For qualifying state-licensed medical marijuana operators, the action may affect federal compliance obligations and Section 280E tax treatment. But the action does not legalize marijuana nationwide, does not automatically include adult-use cannabis businesses, and does not confirm retroactive tax relief or banking changes.

Treasury and IRS have indicated that additional tax guidance is expected. Broader marijuana rescheduling remains a separate pending process.

The safest takeaway is narrow and practical: federal marijuana rescheduling created a limited medical-category Schedule III framework, while several major compliance and tax questions remain unresolved.

Footer

Version: v1.0

Based on verified statutory and regulatory sources current as of April 2026.